Call Buyer Targets Small-Cap Bio C4 Therapeutics (CCCC)

C4 Therapeutics (CCCC) weak biotech recently but saw an interesting buy on 1/10 for 1000 July $35 calls for $5.30 to $5.40 and name that has less than 900 calls in total open interest. CCCC is a $1.42B biotech focused on targeted protein degradation science which they are using to develop next-gen small-molecule medicines. Protein degradation is an interesting new approach to treating areas like cancer but remains in the early stages of development. Proteins are complex molecules within cells that are fundamental for structure of tissues and organs and within the body, cells can regulate the balance of proteins through degradation – the simple removal of proteins. This is a critical process for cell health as is gets rid of unnecessary proteins, damaged proteins, and those that are faulty in any way. And, as a cancer therapeutic process, degradation basically leverages the body’s natural process to instead target and remove pathogenic proteins from the body. This is considered a potentially huge breakthrough in oncology as many proteins (CCCC estimates 85%) are considered ‘undruggable.’

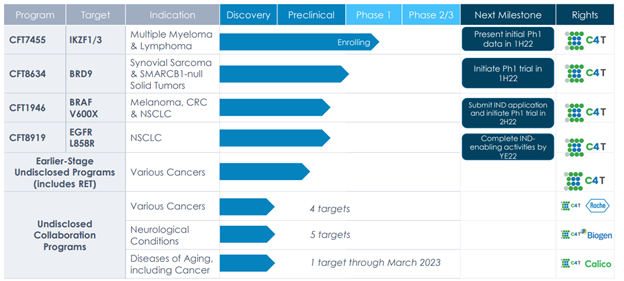

CCCC is utilizing their TORPEDO platform to develop potent, targeted protein degrader medicine and hopes to create a flexible, efficient process that can be repeated across a number of indications. The company has early Phase 1/2 data due in the 1H of 2022 in hematologic malignancies. They also announced a number of milestones at JPM HC on Monday for the year including initiating a number of trials in solid tumors and other indications.

HCW has a $63 PT for shares noting in June that the combination of collaboration revenues, support from partnerships, and validated science provides downside protection in the early years as C4T aims to advance its pipeline through the regulatory process. BAML started at Buy in November noting, “We like C4 for 1) strength of preclinical data package for CFT7455 with best-in-class potential, 2) lower translational risk leading the pipeline programs with validated targets (IKZF1/3 and precision oncology) and attractive market opportunities, and 3) broad-based approach which could better position C4 in drugging intractable targets vs. peers.”

Hedge fund ownership rose 12% last quarter. Driehaus a notable buyer while Perceptive has a 2.2M share position. Short interest is 7%.